Investors Are Ignoring The Evidence At Their Peril

I was recently watching a movie about the FBI trying to bring down a terrorist cell in the U.S. During their investigation, their evidence board became more and more cluttered with people, evidence, and locations as they attempted to track down the “cell.” At first, the clues were disparate, and they didn’t provide a clear path to the end goal. But as more clues were obtained, the bigger picture emerged eventually leading to the successful ending of the terrorist threat.

私は最近こういう映画を見た、FBIが米国のテロ組織をやっつけようとする話だ。捜査段階で、彼らの証拠は各方面に分散していた、そして壊滅しようとする「組織」の場所もだ。当初、手がかりはてんでばらばらだった、そして彼らは結末に向かう道筋を展望できなかった。しかしさらに証拠を積み重ねることで、やがて全貌を把握できるようになりテロリストの脅威を成功裏に取り除いた。

It got me to thinking about what is currently happening in the markets. As stocks rang new highs last week, there were several disparate stories that caught my attention. Individually, each story is nothing to be overly concerned about, and are regularly dismissed by investors. However, when you begin linking these stories, a picture is beginning to emerge that suggests investors may be ignoring the evidence at their own peril.

これをみて私は現在市場で起きていることを考えた。先週も株式市場は新高値の鐘を鳴らし続けるなかで、私が注目する一見無関係の出来事が起きている。個々に見ると、その出来事は全く懸念すべきことではないようにみえる、通常投資家はこんなことを気にかけない。しかしながら、皆さんがこれらの出来事の間の関連に注目すると、大きな絵が見えてくる、投資家は差し迫る脅威を無視しているのではないかと。

Story 1: CPI Remains Weak

話題1:CPIは弱いまま

Despite three hurricanes and wildfires over the last couple of months, core CPI (ex-aircraft) failed to register much inflationary pressure. One would have expected given the surge in demand for goods and services needed to rebuild destroyed communities.

3個もハリケーンの襲来がありこの二ヶ月山火事続きだが、コアCPI(除く航空機)にインフレ圧力は見られない。破壊された地域の復興で物やサービスの需要が急増することを期待した人もいるだろう。

However, despite the Fed’s hopes for a surge in inflationary pressures to justify further hikes in interest rates, inflationary pressures have been on the decline for the last several months.

しかしながら、FEDはさらなる金利引き上げを正当化するためのインフレ圧力を期待しているが、個々数ヶ月その圧力はさがっている。

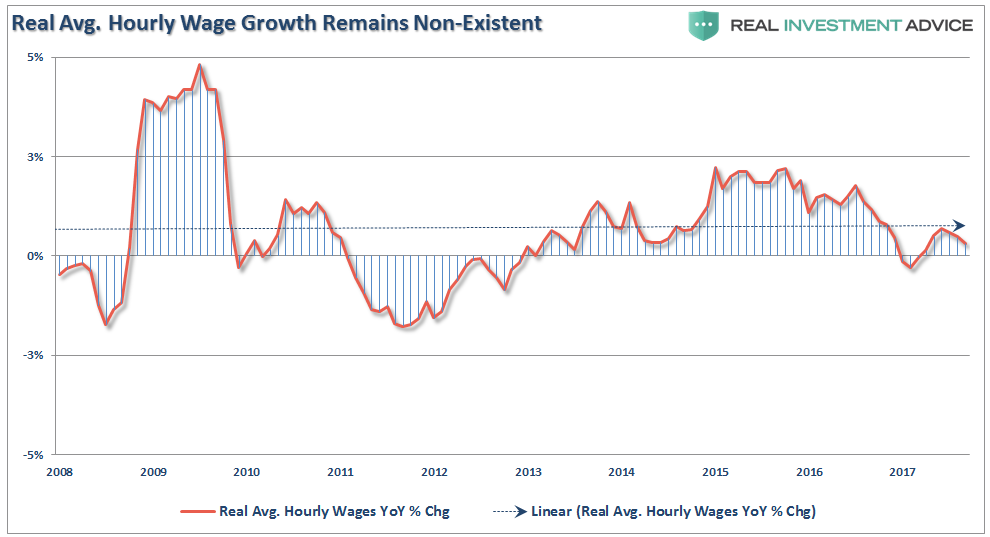

Story 2: Real Wage Growth Slumps Along With Employment

話題2:実給与の伸びは低調、一方で雇用は良好

Of course, the lack of inflation leads through to a decline in inflation-adjusted wages. While the chart below only goes back to 2008, wage growth has been non-existent since 1998. (For more detail read this.)

当然ながら、インフレ欠如のもとでインフレ調整給与も下がっている。下のチャートは2008年以来のものだが、給与増加は1998年以来起きていない(もっと詳細にはここを参照)。

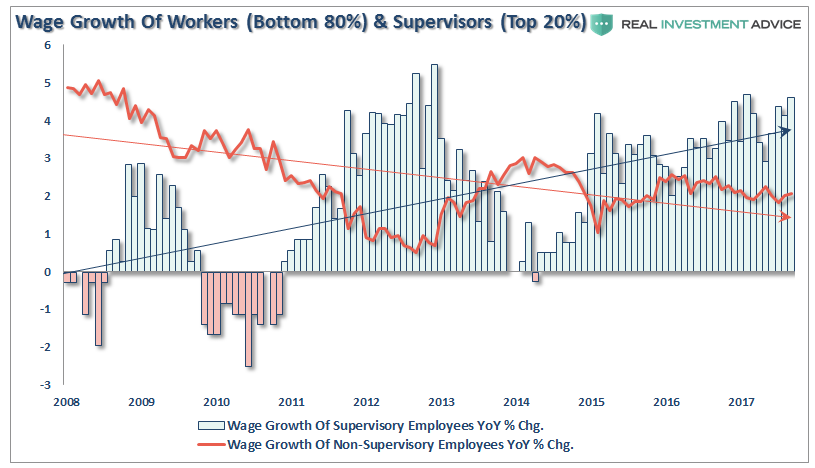

But as I discussed previously, even those wage numbers are skewed by the top 20% of income earners versus the bottom 80% which continue to see wages decline.

しかし以前私が議論したが、これらの給与は上位20%と下位80%の間では歪みがあり、下位の人たちはさらに給与が減っている。

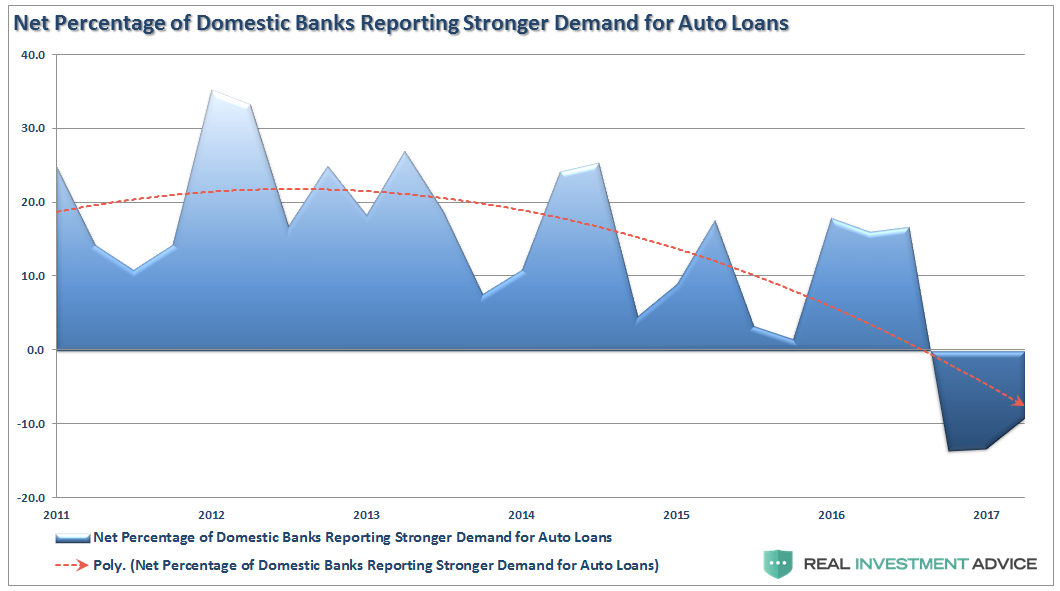

Story 3: Auto Originations Crash

話題3:自動車ローンは急落

As Wells Fargo announced this past week, the decline in auto loan originations continued tumbling 47% Y/Y to only $4.3 billion, the lowest print since the bank started disclosing this item back in 2013.

Wells Fargoが先週報告したが、自動車ローン契約は年率47%下落しわずか$4.3Bとなった、当行がこのデータを開示し始めた2013年以来で最低だ。

The problem is that it is not just Wells having this problem, but all banks. As shown in the chart below the number of banks reporting strong auto loan demand has been in decline for quite some time.

この問題を抱えているのはWells Fargoだけではない、すべての銀行が同様だ。下のチャートを見れば分かるがもう長らく多くの銀行で自動車ローン需要は減退している。

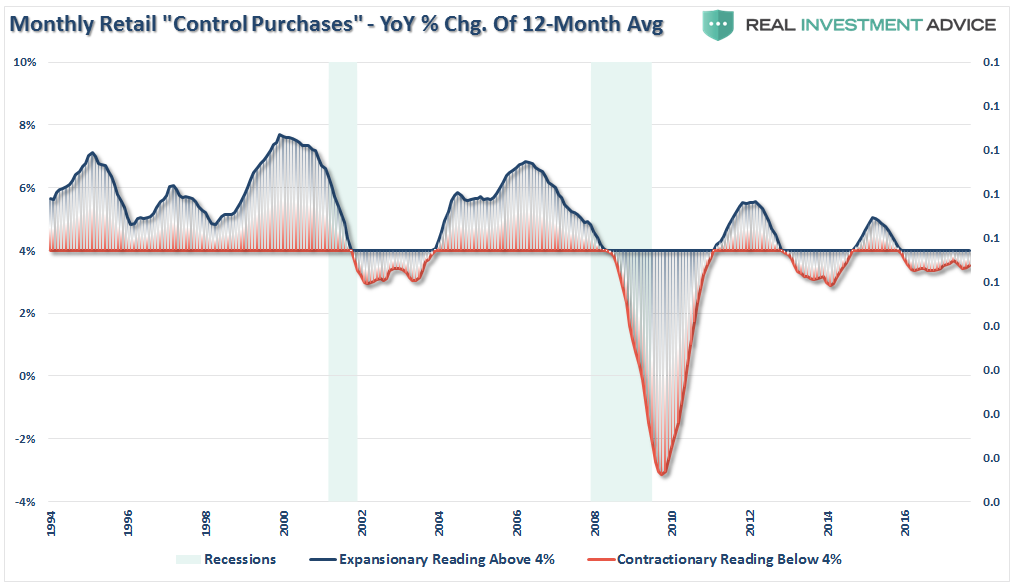

Story 4: Retail Sales Continue To Lag

話題4:小売は引き続き衰えている

It isn’t just auto either. Retail sales account for roughly 40% of

personal consumption expenditures which makes up 70% of the economy. With

wages stagnant, and the real cost of living on the rise, it is not

surprising that with roughly 80% of Americans living

paycheck-to-paycheck that retail sales continue to wane.

減退しているのは自動車だけではない。経済の70%が個人消費に支えられているが、この個人消費の内40%は小売りによるものだ。給与が伸び悩み、そのうえに生活費は上昇している、米国人の80%が次の給与支払いまでをなんとか凌いでいる状況だ、小売は引き続き弱まっている。

The chart below is the annual percent change in the 12-month average of “control purchases.” These are the items that consumers buy with regularity and shows why retail struggles aren’t just related to the “Amazon effect.”

下のチャートは「control purchases」の年率変化を12か月平均したものだ。ここに含まれるのは消費者が日常的に購入する品目で小売店が「Amazon effect」と競合しないものだ。

Story 5: Pay-Tv Customers Decline

話題5:有料テレビ契約者の減少

While “cutting the cord” may be a “thing,” this is much more a story about consumers being faced with a choice between making their mortgage payment or paying for cable. With budgets strained, consumers are actively seeking choices where they can get access to programming at much cheaper costs. From Bloomberg last week:

「cutting the cord」が「象徴的」できごとかもしれない、消費者は住居費を優先するか有料TVを選択するかを迫られている。予算は限られており、消費者は積極的に安いサービスを求めている。先週のブルームバーグ記事ではこういう具合だ:

“Barring a major fourth-quarter comeback, 2017 is on course to be the worst year for conventional pay-TV subscriber losses in history, surpassing last year’s 1.7 million, according to Bloomberg Intelligence. That figure doesn’t include online services like DirecTV Now. Even including those digital plans, the five biggest TV providers are projected to have lost 469,000 customers in the third quarter.”

「Q4に大きな回復がない限り、2017は有料テレビ加入者が歴史的減少となる最悪の年となるだろう、昨年の1.7Mを大きく上回る、とブルームバーグは伝える。この数値にはDirec TV Now のようなオンラインサービスを含んでいない。このようなデジタルサービスを含むと、5大テレビ局はQ3に469,000の視聴者を失った。」

At least all the “low budget” films are getting a shot at a whole new audience. So sit back, grab some popcorn and take in “Galaxina” or “Cannibal Women From The Avocado Jungle.”

少なくとも「低予算」の映画が新たな視聴者をひきつけている。というわけでソファに座りポップコーンを手に、「Galaxina」や「Cannibal Women From the Avocado Jungle」を見ているわけだ。

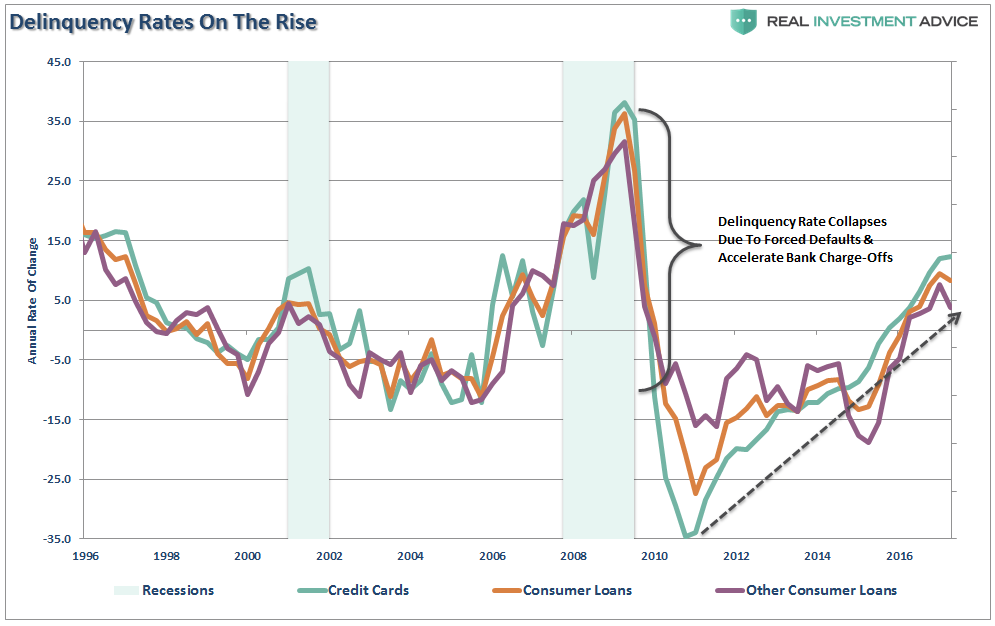

Story 6: Banks Ramp Up Loan Loss Reserves

話題6:銀行は貸倒れ引当金を積みましている

In another interesting note this week, Citi, JP Morgan and BofA all boosted their “loan loss reserves” by the most in 4-years. Banks don’t boost reserves unless there is a rising risk of defaults on the horizon. From Zerohedge:

“Four months ago, when looking at the latest S&P/Experian data, we first reported that credit card defaults had surged the most since June 2013, a troubling development which ran fully counter to the narrative that the economy was recovering and the US consumer’s balance sheet was improving.

「4か月前のことだ、最新のS&P/Experianデータを見た時、ZeroHedgeは最初にこう報告した、クレジットカード不履行が急騰しており2013年6月以来のものだ、カードトラブルが増えているということは経済回復で米国消費者のバランスシートが改善しているという一般的なお話とは相反する。

The troubling deterioration prompted Moody’s to pen its own report titled ‘Spike in Charge-off Rates Indicates a Slide in Underwriting Standards’ and as Moody’s analyst Warren Kornfelf wrote, the steep increase in credit card charge-off rates in 1Q’17 and 4Q’16 was the largest since 2009, and indicates that ‘strong underwriting standards in place since the financial crisis have deteriorated, potentially rapidly.'”

トラブルが悪化する状況で Moodysはこういう記事を出した「貸倒れ償却が急騰するということは貸出基準の劣化を示す」そしてMoodysのアナリストWAっレンKornfelfはこう書いた、クレジットカードの貸倒れ急増が2017Q1と2016Q4に起きており、2009年以来で西田のものだ、ということは「金融危機以来の厳しい貸出基準も不十分ということだ、急速に悪化している。」」

Of course, the following chart might just suggest why they are doing that.

当然のことながら、下のチャートをみるとその状況がわかるかもしれない。

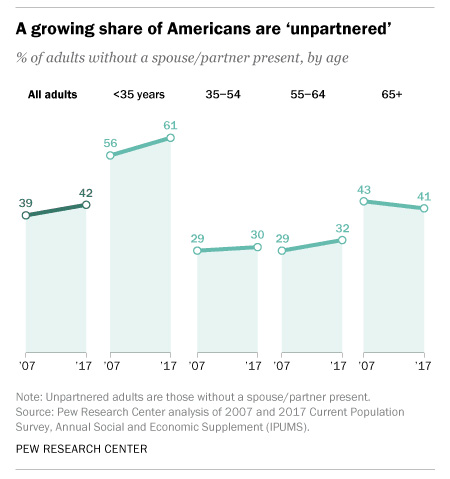

Story 7: Millennials Are Delaying Marriage Because Men Aren’t Earning Enough

話題7:若者は結婚を遅らせている、その理由は男性の稼ぎが充分でないからだ

As reported by The Hill this past week, more Americans are living alone today has risen sharply.

先週、The Hill が報告したが、独身米国人が急増している。

“The number of Americans living with a spouse or partner has fallen notably in the last decade, driven in part by decisions to delay marriage in the wake of a recession that hit new entrants into the workforce especially hard.

「この10年、配偶者と暮らす米国人が急減しえいる、景気後退後新たに雇用市場参入が難しくなったことが結婚を遅らせている。

Forty-two percent of Americans live without a spouse or partner, up from 39 percent in 2007, according to the Pew Research Center’s analysis of U.S. Census Bureau figures. For those under the age of 35 years old, 61 percent live without a spouse or partner, up 5 percentage points from a decade ago.”

米国人の42%に配偶者が居ない、2007年には39%だったのにこれが増えている、米国統計局のPew Research Centerの調査による。35歳以下では61%に配偶者が居ない、10年前から5%増えている。」

With more multi-generational families living together, the aging of the baby-boomer generation and a significant fall-off in birth rates, the huge demographic headwind is gaining momentum. The economic ramifications, as well as for the financial markets, is going to be extremely problematic. (Read this.)

多世代家族が増えており、ベビーブーマーが年をとり出生率が大きく減っている、人口動態に大きな向かい風が吹いている。経済や金融を取り巻く不確実性が大きく問題になっている。

Tying It All Together

すべてを勘案すると

As more clues become available, the risk to the financial markets becomes clearer.

多くの手がかりを得ることで、金融市場におけるリスクが明らかになってきた。

All of these stories have a common thread – the consumer. While stocks continue to ratchet to all-time highs on expectations of tax cuts and reforms leading to stronger economic growth, the stories here all suggest something much more telling is happening beneath the surface.

ここで取り上げた話に共通するのはーー消費だ。株式市場は減税期待と経済再生による経済成長期待で新高値を続けているが、ここで取り上げた話はどれも表面化で起きている大きなうねりを示唆するものだ。

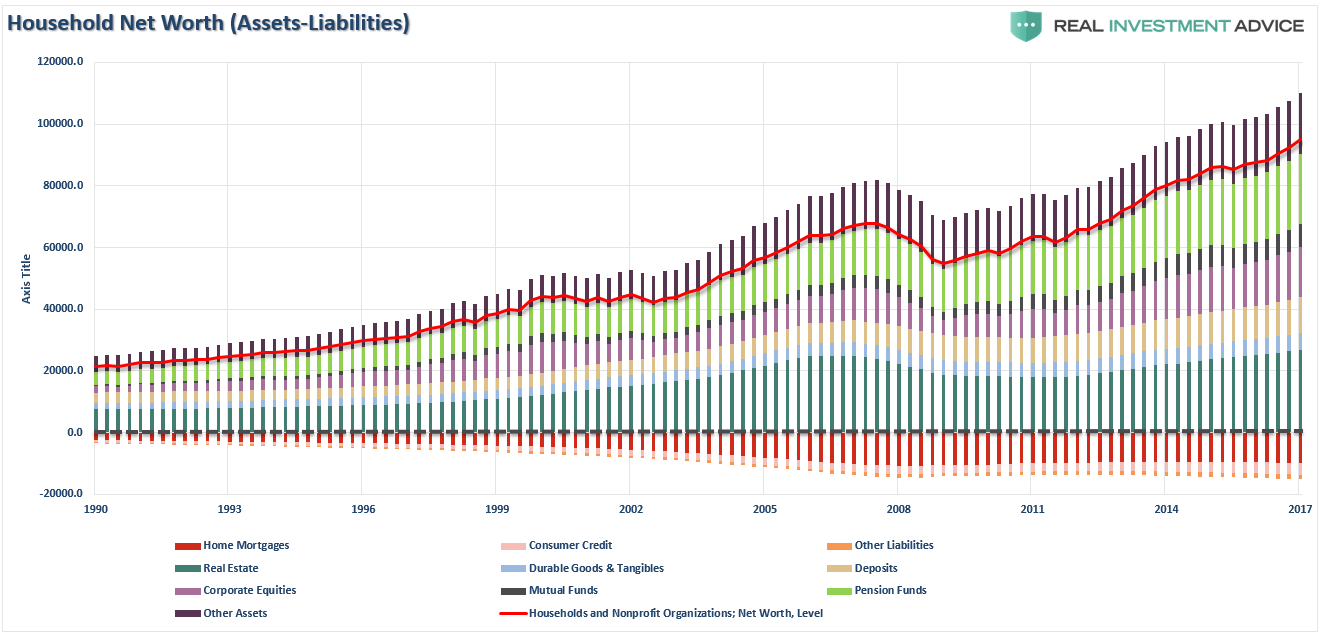

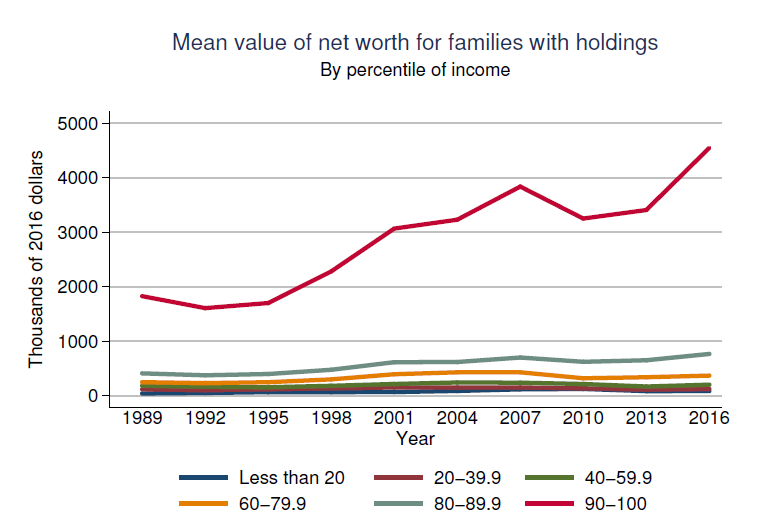

Yes, household net worth has recently reached historically high levels. However, The majority of the increase over the last several years has come from increasing real estate values and the rise in various stock-market linked financial assets like corporate equities, mutual and pension funds.

そう、家計資産は最近過去最高になってきた。しかしながら、ここ数年の家計資産増は主に不動産評価の高まりと株高によるもので、株式、投資信託そして年金基金のようなものだ。

But, once again, the headlines are deceiving even if we just slightly

scratch the surface. Given the breakdown of wealth across America we

once again find that virtually all of the net worth, and the associated increase thereof, has only benefited a handful of the wealthiest Americans.

しかし、繰り返すが、ちょっと深掘りすると新聞の見出しは騙しにすぎない。米国人の資産の内容を詳しく見てみると、ほとんどすべての資産は、確かに増えているが、一握りの豊かな米国人の手の中にある。

As the Federal Reserve just recently reported, while the mainstream media continues to tout that the economy is on the mend, real (inflation-adjusted) median net worth suggests this is not the case overall. As stated, the recovery in net worth has been heavily skewed to the top 10% of income earners.

FEDがつい最近報告したことだが、主要メディアは引き続き経済は回復していると伝えるが、実際の(インフレ調整後の)中央値のひとの資産はこれには当てはまらない。FEDが言うとおり、景気回復の恩恵を受けているのは収入が上位10%の人たちだ。

Of course, this explains why the largest number of the population over the age of 65 is still employed as they simply can’t afford to retire. The multi-generational households are on the rise, not by choice but by necessity. These are long-term headwinds that suggest economic growth will remain weak, and the rise in delinquencies, slow-down in auto demand, and weak retail sales all suggest consumers may have reached the limits of the debt-driven consumption cycle for now.

当然のことながら、これをみると理解できるが、65をすぎた人の多くが働いておりその理由は単に引退できないというだけだ。多世代家庭が増えており、それは望んでいるわけではなく、必要に迫られているのだ。これらは長期的には経済成長に向かい風となり、弱い成長となるだろう、そして債務未払いや自動車ローン減退、そして弱い小売を見ると消費者はすでに債務による消費拡大の限界に達していると言える。

In other words, individuals are ratcheting up debt, not to buy more stuff, but just to maintain their current “standard of living.”

言い換えると、個人消費者は債務を積み増し、これ以上消費できず、単に現在の「生活水準維持」にきゅうきゅうとしている。

The disconnect between the stock market and real economic growth can certainly continue for now. Exuberance and confidence are at the highest levels on record, but the underlying stories are beginning to weave a tale of an economy that is very late in the current cycle.

株式市場と実経済成長の乖離がいま進行中だ。株式市場の活力と信頼は記録的な高みに有る、しかしその背景をみるとこの景気サイクルの最終局面が見て取れる。

Importantly, these are not short-term stories either. The long-term

picture for the economy and the markets from the three biggest factors (Debt, Deflation, and Demographics) continues to build. These

factors will continue to weigh on economic growth, and market returns,

during the next generation as the massive wave a baby-boomers shift from

supporters to dependents of the financial and welfare system.

大切なことは、ここに述べたことは短期的な話ではない。経済の長期視点と市場の三大要因(債務、デフレ、人口動態)が引き続き積み上がっている。これらの要因は引き続き経済成長と市場リターンの重しとなる、団塊の世代が金融や福祉分野でこれまでのサポーターから依存社にシフトしている。

As an investor, it is important to pay attention to the clues and the weight of the evidence. The success, or failure, of catching the end of the current bull market and economic cycle will have important implications to your long-term financial goals.

投資家としては、各種手がかりや証拠に目を向けることは大切なことだ。現在の経済サイクルにおける終点を捕まえるか見逃すかは皆さんの長期金銭ゴールにとってとても大切なことだ。