Dangerous Markets - Signs, Signs, Eveywhere A Sign

Last week, I noted:

先週、私はこう書いた:

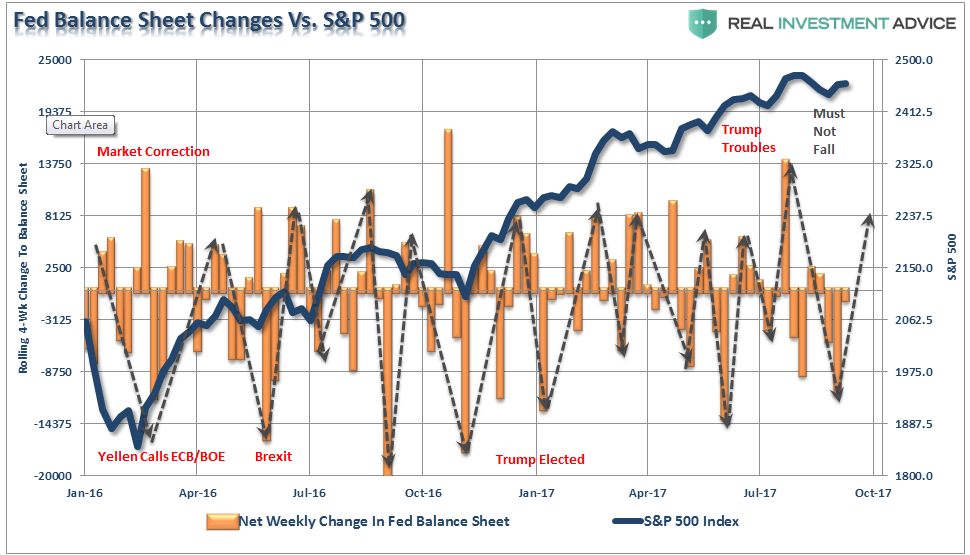

“I have a sneaky suspicion that when I update the Fed Balance Sheet reinvestment analysis next week, shown below, we are going to find a substantial, well-timed, reinvestment by the Central Bank. Wanna bet?”

「私は密かに疑っている、私が次にFEDバランスシートの再投資を来週点検すると、それはこれからわかるが、かなりな量を再投資しているのではないかと。賭けても良い?」

Well, here is the updated chart of the 4-week net change to the Fed’s balance sheet. As you can see, reinvestments have, once again, returned to the market in a very “timely” fashion. Of course, since the Fed claims they are not trying to, nor are they influenced by, the markets, this is purely coincidental. (#SarcasmAlert)

そう、下に示すのがFEDバランスシートのここ4週の変化だ。見ての通り、再び再投資がとても「都合よく」行われている。当然、FEDは意図したものではないという、ましてや市場をみて行動しているわけでもないと、でもまったく同期している(#SarcasmAlert)

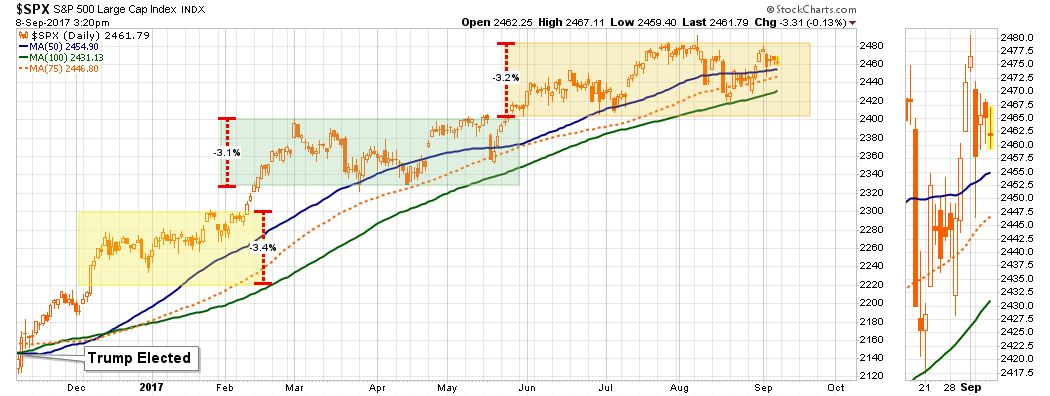

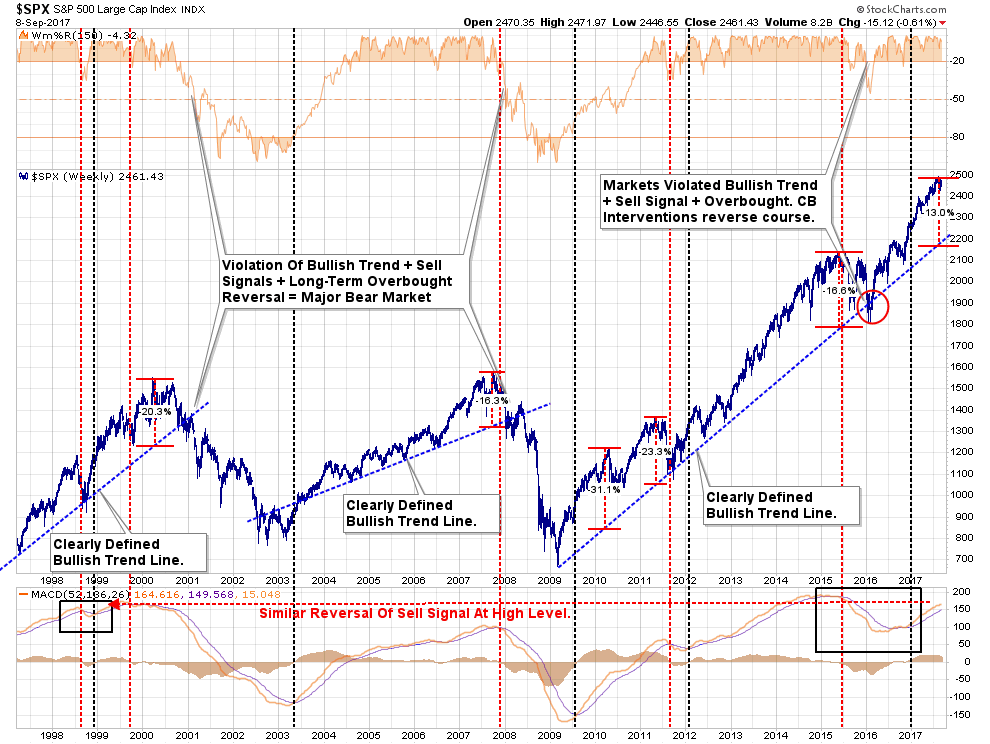

The good news this week is that the market maintained last week’s advance despite the one-day tantrum earlier this week. Interestingly, since the election, the market has ratcheted higher in slightly more than 3% increments with each move higher followed by a drawn-out consolidation process that runs primarily along the 50-75 dma. The last sell-off tested, and held, the 100-dma but stayed within the confines of the consolidation process. The 2400 level on the S&P 500 remains the clear “warning level” for investors currently.

良い知らせは、市場は先週の快調を持続している、癇癪を起こしたのは週初めの一日だけだ。面白いことに、選挙以来、市場は値固めごとに3%増加している、これは40−75日移動平均に添っている。直近の下落では下値を試されたが100日移動平均は維持した、値固めの範囲内だ。現在のところ、S&P500は2400が明らかな「警告レベル」と投資家にみなされている。

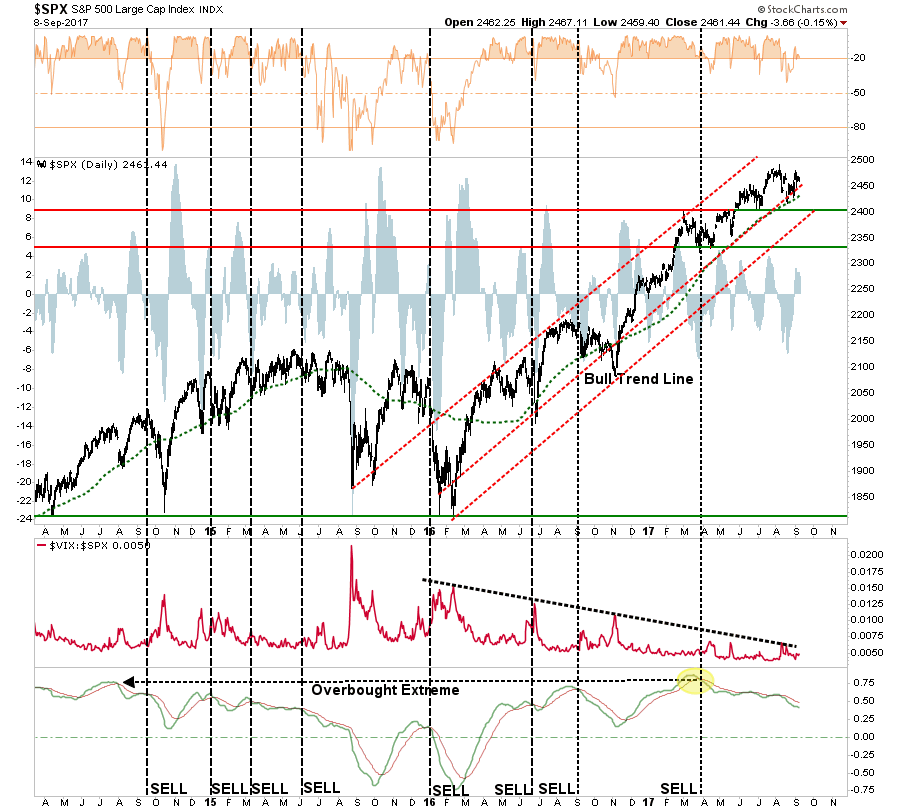

But this short-term bullish backdrop is offset by intermediate-term bearish underpinnings as shown by the next two charts. With an intermediate-term momentum sell-signal in place, combined with overbought conditions, continues to suggest further gains from this point will likely remain limited and more volatile to obtain. That statement DOES NOT preclude the markets reaching new highs, it just suggests that downside corrective risks outweigh the potential currently for further gains.

しかしこの短期的な強気の背景には中期的なベア相場背景が潜んでいる、次の二枚のチャートを見るが良い。中期的な視点でモメンタムを見ると売りシグナルがでている、買われすぎなのだ、現時点からのさらなる上昇には限界があり、さらなるボラティリティを示唆している。この状況は市場が新高値となることを妨げている、チャートの示唆するところは、さらなる上昇よりも下落調整の可能性が高い。

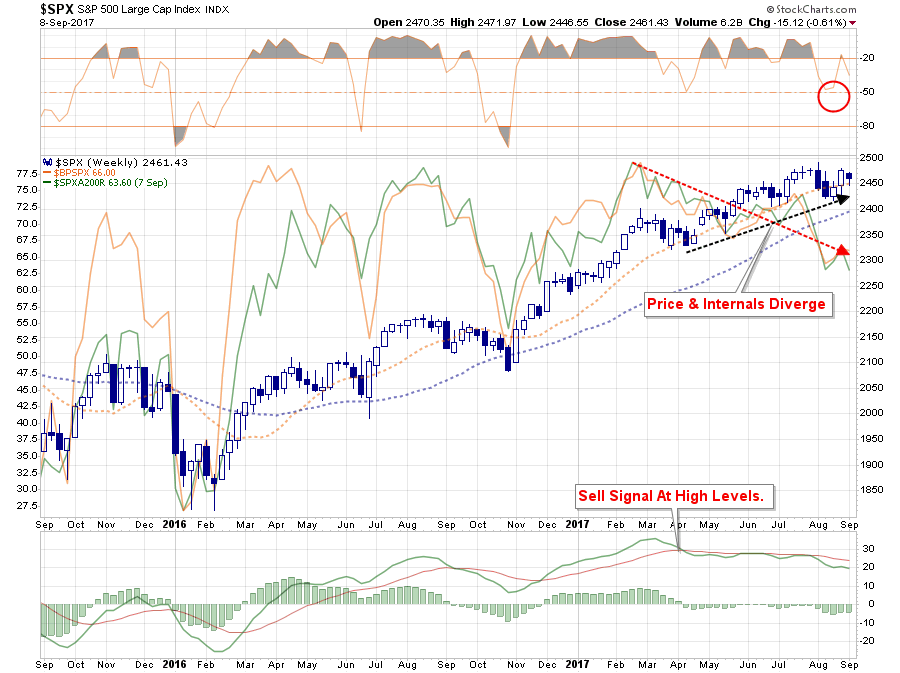

The bigger concern continues to be the internal deterioration of the markets as the number of stocks on bullish “buy signals” and the number of stocks above their 200-dma continue to deteriorate. Again, this is more supportive of a continued correctionary process versus a reversal and strong push higher in asset prices.

より大きな懸念は、市場内部が劣化していることだ、強気で「買いシグナル」を発する銘柄の数や200日移動平均を上回る銘柄の数が減っている。繰り返すが、現状は調整の可能性のほうが反騰の可能性よりも懸念される。

Importantly, as I will discuss momentarily, there are technical

similarities suggesting we could be closer to the next major market

reversal than not. While the markets are currently on a longer-term “buy signal,” as shown at the bottom of the chart below, the current signal is similar to what was seen in the run up to the peak of the “dot.com” bubble.

大切なことは、これから議論するが、テクニカルを見る限りでは次の大きな市場反転を示唆している、さらなる上昇ではない。市場は現在長期的な「買いシグナル」を発して入るが、下のチャートの株を見ればわかるが、今のシグナルは「ドットコムバブル」で天井間近のときとよく似ている。

Notice that in 1998, the “buy signal” was reversed temporarily by a sharp sell-off in the market due to the collapse of “Long-Term Capital Management.” A test of the “bullish” trend held and the markets reversed as the “dot.com” bubble ensued. The next “sell signal” denoted the beginning of the market topping process and prices followed soon thereafter.

1998年を思い起こしてほしい、「買いシグナル」は市場の急落ですぐに反転した、その原因は「LTCM」の倒産だった。「ブル」トレンドは続いていたが、「ドットコムバブル」のあとに市場は反転した。次の「売りシグナル」は市場の天井形成の始まりだった、そして株価はすぐにそれに従った。

With a large deviation from the bullish trend, combined with a long-term signal at very high levels, the next reversal that violates the bullish trend will very likely signal the beginning of a more protracted bear market.

ブルトレンドからの大きな乖離を伴い、とても高いレベルでの長期シグナルであることを勘案すると、ブルトレンドを打ち砕く次の反転は長期的なベアマーケットの始まりとなりそうだ。

The warning signs are stack up on a technical basis suggesting the “risk” is becoming more elevated.

チャートテクニカルからは警告シグナルを発しており、これは「リスク」の高まりを示唆している。

While the bullish trend remains intact, keeping portfolios allocated toward equity risk currently, we are more focused on rebalancing and hedging risk in portfolios currently.

強気トレンドが持続しポートフォリオは現在のリスクに対応したままだが、我々は現在のポートフォリオをリバランスとリスク回避に注意を向けるべきだ。

We agree with Howard Marks who recently stated:

私も最近のHoward Marksの主張に同意する:

“It’s time for caution, not a full-scale exodus.“

「注意すべき時だ、ただし全力脱出ではない。」

Yet.

まだだ。

As for what to do right now, we are pursuing the same strategy he discusses in his latest missive:

今やるべきことは、彼の最新の手紙と同じ戦略を我々も取っている:

“Thus I would mostly do the things I always have done and accept that returns will be lower than they traditionally have been. While doing the usual, I would increase the caution with which I do it, even at the cost of a reduction in expected return. And I would emphasize “alpha markets” where hard work and skill might add to returns, since there are no “beta markets” that offer generous returns today.

「しかるに私はいつもと同様のことをしようと思う、そしてこれは了解している、今の市場からかつて程のリターンは期待できない。いつものとうり、私はより注意深く行動し、予想収益低下に手間をかける。そして私は「市場のアルファ」に重点を起きたい、ただしこれには労力とスキルを要する、というのもいまや「市場のベータ」は期待できないからだ。

‘Move forward, but with caution.'”

「前進しよう、ただし注意深く。」」

Signs, Signs, Everywhere A Sign

ここにもそこにもいたるところに兆候がある

You don’t have to look very hard to see a rising number of signs that suggest the “Trump Trade” has come to its inevitable conclusion.

「トランプトレード」の帰結について多くの示唆が増えていることを発見するのにそう手間はかからないだろう。

Following the election, this past November the financial markets rallied sharply on the hopes of major policy reforms and legislative agenda coming out of Washington.

選挙以来、金融市場はラリーを続けた、大きな政策変更法案成立がワシントンから出てくると期待してのことだ。

Eleven months later, the markets are still waiting as the Administration has remained primarily embroiled in Washington politics with a divisive, Republican controlled, House and Senate. While there are still “hopes” the Administration will pass through tax reform, the failure to “rally the troops” to repeal the Affordable Care Act leaves permanent tax cuts an unlikely outcome. That hopeful outcome was further exacerbated with the deal cut between President Trump and leading Democrats to lift the debt ceiling and fund the Government through December. That “deal” has effectively nullified any leverage the Republicans had to strong-arm a deal on taxes later this year.

すでに11か月を経過したが、政権はワシントンの政治家と論争している、上院下院ともに共和党が取っているにも関わらずだ。いまだに政権への「期待」が残るのは税制改革だが、

オバマケア修正に「意見一致」をみることもできない、これで永続的な税制改革ができるとは思えない。債務上限を巡っては民主党とトランプ大統領はさらに関係悪化しそうだ、12月まで一時的に先延ばししたにすぎない。この「ディール」は税制改革に関する共和党の主張を無力化した。

The markets are figuring it out as well.

市場もこのことを折り込みつつある。

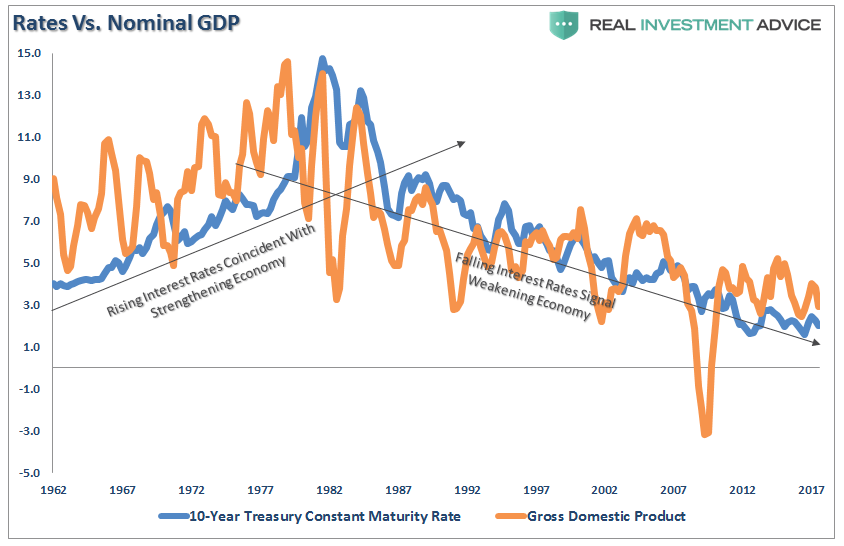

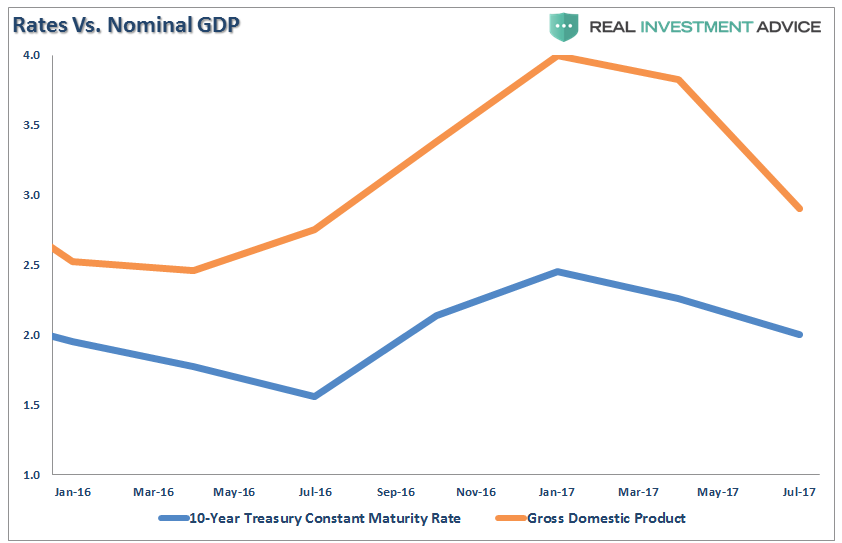

If you want to know where the economy is headed over the next few months, you don’t have to look much further than interest rates. Since interest rates are ultimately driven by the demand for credit, and that demand is driven by economic growth, their historical correlation is no surprise.

もし今後数ヶ月経済の行く末を知りたいと思うなら、金利を見てはいけない。金利というのは本来資金需要に依存するもので、この需要は経済成長に伴う、経済成長との歴史的相関をみても驚くことではない。

But like I said, if you want to know where GDP is going to be

in the months ahead, keep a close watch on rates. I suspect, before

year-end, we will see rates below 2.0%.

しかし私が言ったように、今後数カ月のGDP動向を知りたいなら、金利に注目すると良い。私が思うに、年末まで、金利は2.0%以下だろう。

As a reminder, this is why we have remained rampant bond bulls since 2013 despite the continuing calls for the end of the “bond bull market.” The 3-D’s (Demographics, Deflation & Debt) ensure that rates will remain low, and go lower, in the years to come. Think Japan.

覚えておいてほしいが、2013年以来債券にブル相場が蔓延している、「債券ブル相場」はもう終わりだと何度もいわれながら。3つのD、(Deomographics, Delfation & Debt,人口動態、デフレ、負債)により金利は抑えられ、さらに低くなっている、これから何年もだ。日本を見るが良い。

But I digress.

ちょっと本題からそれた。

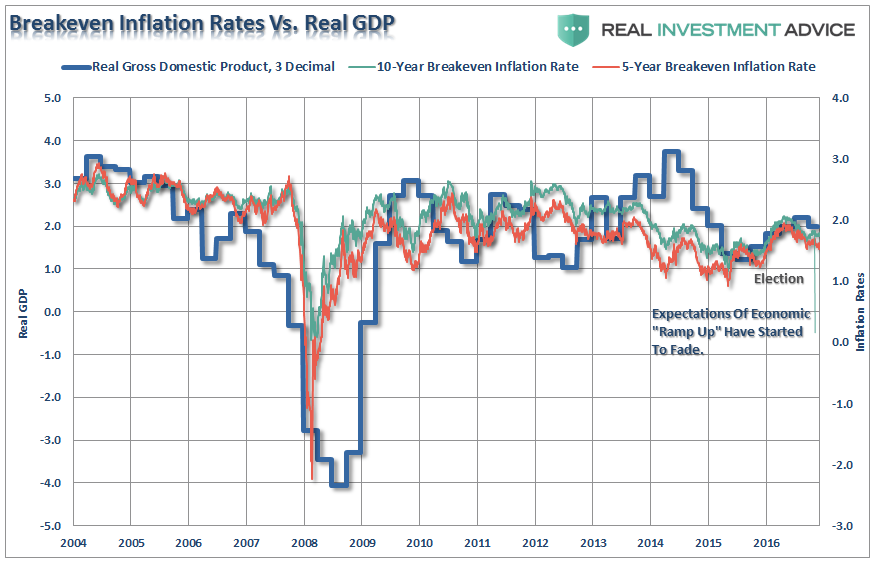

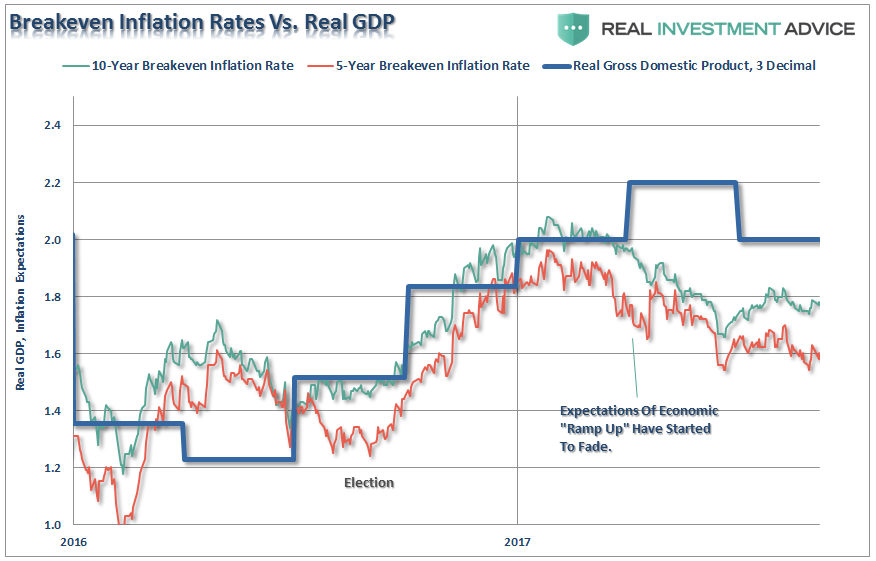

Like rates, inflation is also closely tied to the direction and trend of economic strength. While the Fed continues to hope for a return of inflationary pressures, the real strength of the underlying economy suggests something quite different.

金利と同様にインフレ率も経済成長と密接に関連している。FEDはインフレ圧力をずっと期待しているが、その背景にある実経済は全く異なることを示唆している。

Again, following the election inflationary pressures surged on “hopes” of the “second coming” of the economy. Those hopes are now fading, and economic growth along with it.

繰り返しになるが、選挙後のインフレ圧力は経済への「キリスト降臨」を「期待」してのものだった。この手の期待はいまや消え失せつつある、そして経済成長もそれにともなう。

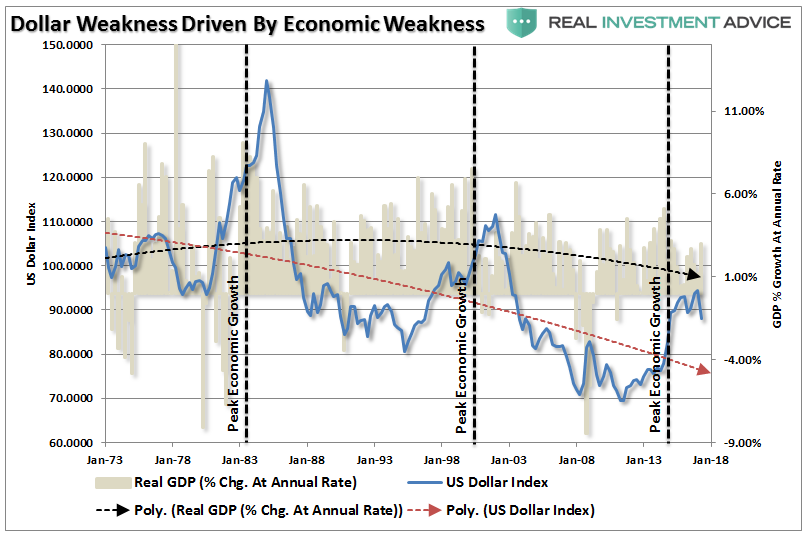

But there is no better sign to watch than that of the US Dollar. The dollar is the representation of the world’s belief in the strength of the U.S. economy. A stronger economy attracts capital and investment which drives the dollar higher and further boosts economic growth. The opposite also applies.

しかし米ドルをみても良い兆候はない。ドルは世界の米国経済への信任を表す。強い経済は資金や投資を呼び込みドルを高くしさらなる経済成長を引き起こす。いまはこの逆だ。

The recent decline in the dollar, which is likely to continue, suggests that economic growth will weaken in the months ahead.

最近のドルの下落、これが継続するように見える、ということはここ数ヶ月経済成長は弱いことを示唆している。

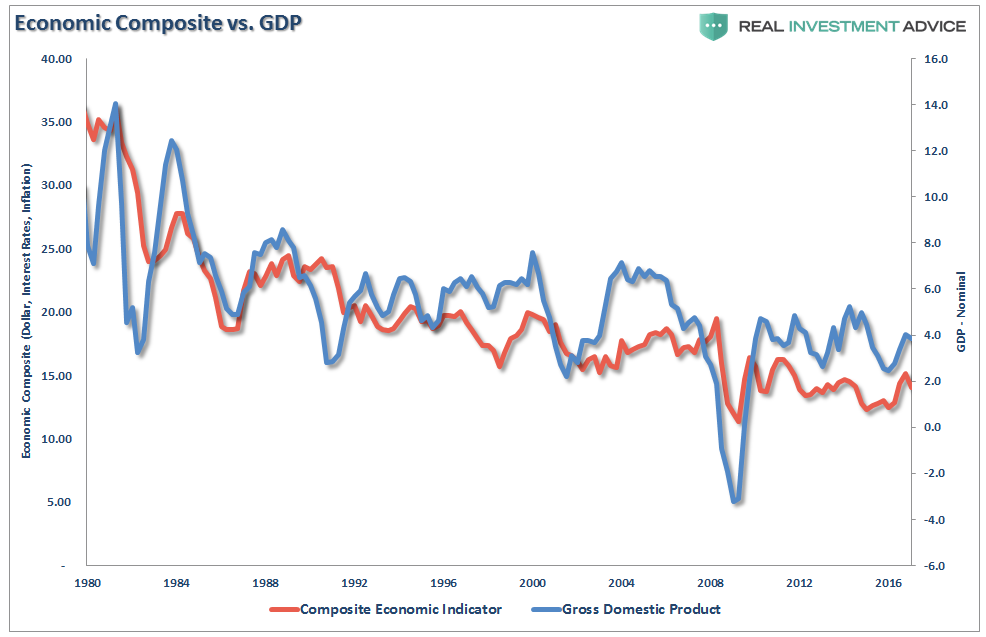

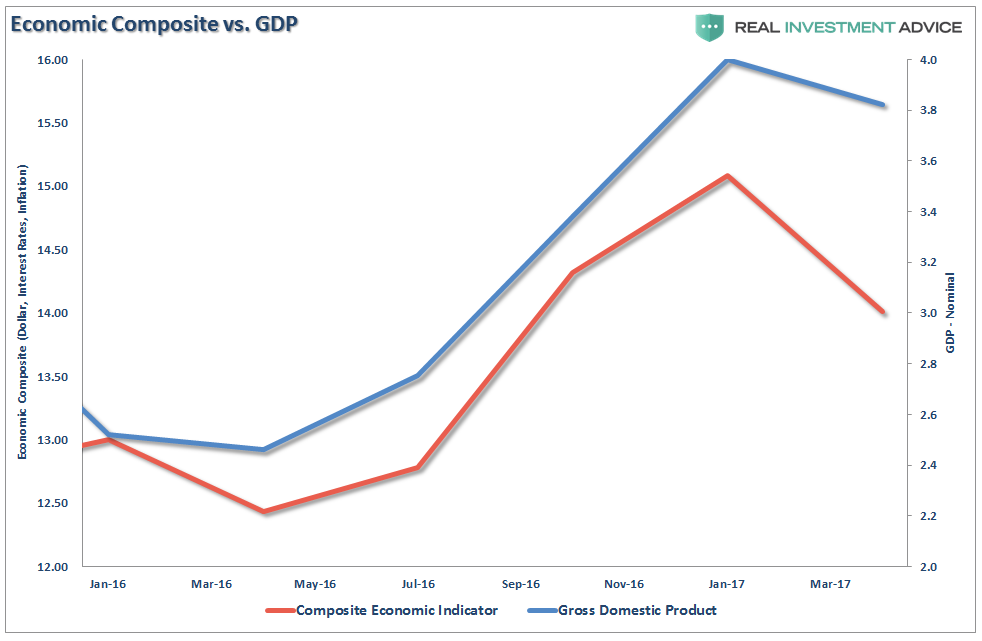

While it is not hard to see, or understand, the correlation between these individual “signs” and the direction of the economy, we can see it even more clearly by building a simple composite. The composite below is the dollar, interest rates, and inflation as compared to nominal GDP.

これを確認氏理解するのは難しくないが、これらの個別「兆候」と経済動向の相関に関し、簡単な経済指標を見るともっと明確にわかる。下の指標は、ドル、金利そしてインフレを考慮したもので、これを名目GDPと較べている。

Currently, the composite index has turned down rather sharply and we should expect economic growth, to track along with it in the coming months.

現在、この指数かなり急激に下落している、ということで経済成長もそれに伴うだろう、今後数カ月の見通しだ。

All of these signs are worth watching closely. A weaker economy leads to weaker earnings growth and estimates are already under rather severe downward pressure. Given the overvaluation of the market, and hopes of legislative agenda beginning to fade, there is a significant risk to outlooks for the market in the months ahead.

これらの指標を注意深く見守るべきだ。弱い経済は弱い利益成長となり深刻な下落圧力となる。市場は過剰評価されており、法案成立期待も消え失せつつある、今後数カ月の市場概況には大きなリスクがある。

The last few times the dollar, rates, and inflation fell following a previous advance, the outcome for investors was not all that great.

最近の、ドル、金利、インフレ後退時には投資家の成績は良いものではなかった。

However, as I said above, we are indeed moving forward, but with caution.

しかしながら、私が既に述べたが、前進しよう、ただし注意深く。

“Here’s your sign.” – Bill Engvall

「あなたにも兆候が見えるだろう。」ーーBill Engvall