The Psychological Impact Of Loss

For the third time in four weeks, the market was closed on Monday due to a holiday. Not only is this week shortened by a holiday, it is also coinciding with the annual Billionaire’s convention in Davos, Switzerland and the Presidential inauguration on Friday. Increased volatility over the next couple of days will certainly not be surprising.

この4週のうち三度市場は月曜が休場だった。今週は祝日で営業日が一日少ないだけでなく、ダボスで大金持ちの年会がある、そしてまた金曜には大統領就任式だ。これからの2日変動が大きくなっても驚くことはない。

In this past weekend’s missive, I discussed a variety of “extremes” being registered in many areas of the market and particularly in prices. To wit:

以前に記事にした週末読み物で、私はいくつかの方面での市場の「過剰」な動きについて議論した、特に株価についてだ。こういうふうにだ:

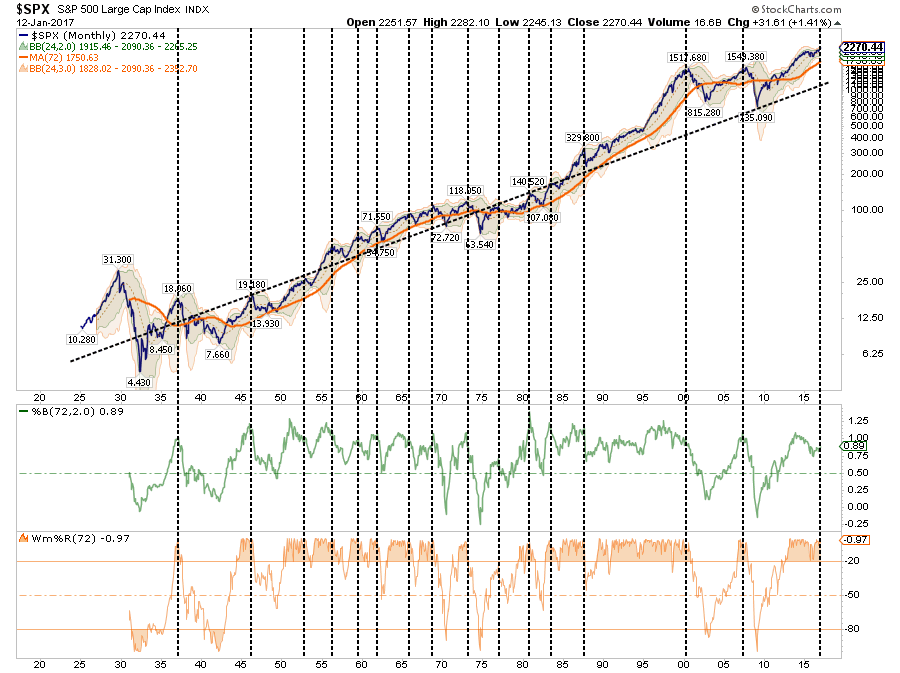

“I have often compared market prices to the equivalent of “stretching a rubber band.” Prices can only deviate so far from the long-term trend line before a mean reverting event eventually takes place. Much like a “rubber band,” prices can only be stretched so far before having to be relaxed to provide the ability to be stretched again.

「私はよく市場価格を「ゴムバンドの伸び」に例える。株価は長期トレンドの上下に変動し平均回帰を行う。これは「ゴムバンド」に似ている、株価は伸びきるためには緩める必要がある。

The chart below shows the long-term trend in prices as compared to its underlying growth trend. The vertical dashed lines show the points where extreme overbought, extended conditions combined with extreme deviations in prices led to a mean-reverting event.”

下のチャートは株価長期トレンドとその背景となる成長トレンドと比べるために示している。縦の点線は極端な買われ過ぎが起きた時点を示す、価格の極端な乖離が平均回帰を起こすときだ。」

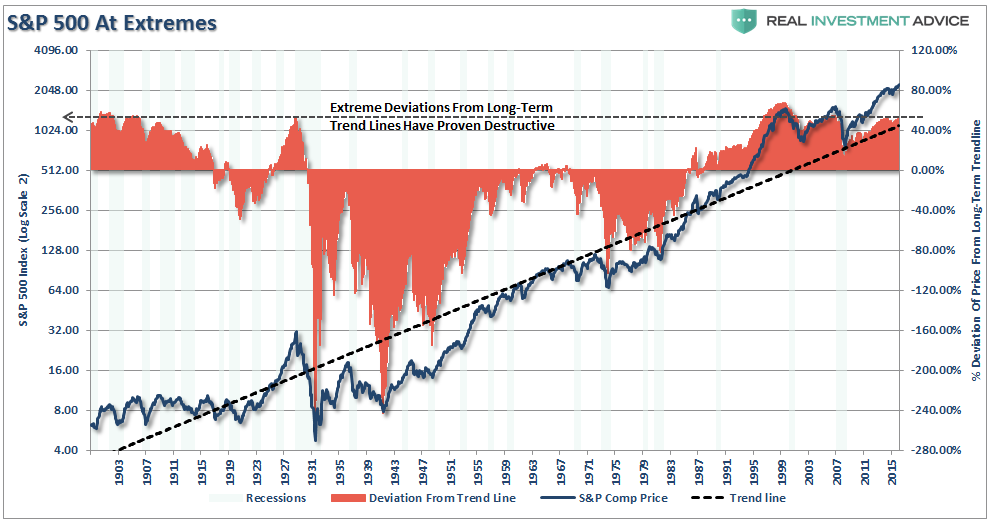

“This is shown a bit clearer below which compares the deviation of the S&P 500 from the long-term growth trend. Currently, while only slightly below the peak of the 2000 “dot.com” bubble, the deviation is at levels that have ALWAYS coincided with a negative mean reverting event or very poor, and highly volatile, forward returns.”

「この図は下のチャートに変換するともっと明確になる、S&P500の変化と長期成長トレンド比較だ。現在は、2000年の「ドットコムバブル」ピークよりもちょっと下で、乖離はマイナス回帰が怒らんとする時点だ、というかとても不安定で、将来のリターンの可能性はとても薄い。」

I know…I know. As soon as I wrote that I could almost hear the cries of the “perma-bull” crowd exclaiming “how many times have we heard that before.”

そりゃわかってる、いつものことだ。私がこう書くと「常時強気派」からは、こういう声がいつも聞こえてくる、「この話はこれまで何度聞いたことか。」

They would be right. The problem with the majority of analysis, in my opinion, is the mismatch between long-term analysis and short-term time frames. The problem with long-term price analysis is the failure to predict short-term price changes. However, short-term analysis leads to psychological wear where analysts have spotted “Head and Shoulder” formations, “Hindenberg Omens,” and “Puppy Monkey Baby“ patterns that have failed to predict a market change.

彼らがそういうのももっともだ。私が思うには、多くのアナリストの問題点は、長期分析と短期的分析を混同していることだ。長期的株価分析は短期的な変動を無視している。しかしながら、短期的分析では心理的な要因を利用するたとえば、「Head and Shoulder 三尊」形成とか、「Hindenberg Omen」、そして「Puppy Monkey Baby」パターンのようなものだ、どれも市場変化など予測できるわけがないのに。

Of course, like “crying wolf,” when these short-term patterns and long-term prognostications fail to immediately validate themselves, they are summarily dismissed as being wrong, or just “mumbo jumbo,” which often leads to unwanted outcomes.

当然のことだが、「オオカミ少年」のようにこれらの短期的なチャートパターンや長期的予言は役に立たないことがすぐ解る、こういうたぐいのものは悪影響したかないことで捨て去られる、もしくは「おまじない」のように扱われて予想外の結論を引出す。

The primary problem is the “duration mismatch” between most technical analysis, which is typically very short-term (minute, hourly, daily), and the outlook for investors which is in years.

As a portfolio manager, what is important for me is the understand the longer-term “TREND” of market prices. By looking at weekly and monthly data, the trend of prices is revealed allowing for a better match between portfolio goals and related market risks.

最大の問題は多くのチャート分析は「時間フレームを考えないことだ」、多くは短期的な(分足、時間足、日足)で、投資家は年単位で物事を考える。ポートフォリオマネージャとして私が重視するのは長期的な市場価格の「トレンド」をを理解することだ。週足、月足をみることで、ポートフォリオの最終目標と関連する市場のリスクをより理解できるようになる。

During “bull markets,” prices are in a steady advance with corrections to the longer-term bullish trend presenting buying opportunities. When prices become extended from the trend, such deviations provide opportunities to take profits and rebalance portfolios.

「ブル相場」の間は、株価は多少の調整を含みながら長期的に増えて行き、押し目は買いの良い機会となる。株価がトレンドを越えたとき、その乖離は利益確定の機会でありポートフォリオリバランスの良い機会だ。

Conversely, during “bear markets,” prices are in a steady decline with corrections to the longer-term bearish trend presenting selling, hedging, and shorting opportunities. When prices become extended away from the bearish trend, such deviations should be used to take profits in short positions and portfolio hedges.

逆に言うと、「ベア相場」の期間は、調整を伴いながら株価は下落をつづける、この際の調整はショートの良い機会となる。株価がベアトレンドから乖離した時、この乖離は空売りの良い機会だ。

This idea is shown in the chart below.

このアイデアは下のチャートに示されている。

By using a 72-week moving average, the longer-term trend of prices is more clearly revealed. As stated, corrections to the longer-term trend during bull markets were buying opportunities, whereas during bear markets they were selling/shorting opportunities.

72週移動平均でみると、株価の長期トレンドが明確になる。すでに述べたが、ブル相場の長期トレンドの中の調整は買いチャンスだ、一方ベア相場では売り/空売りチャンスとなる。

VERY IMPORTANTLY – note that at the peak of the previous two markets the change from a bullish to a bearish trend was denoted by the following price action:

超重要ーー過去二回の市場の変化、ブルからベアへ、は以下のような価格動向で起きている:

- A break of the long-term moving average

- A rally back to the long-term moving

- A failure and a move lower in price than the most recent bottom.

- 長期的移動平均からの乖離

- 長期移動平均への逆行

- 直近の底値割れ

While this occurred at the beginning of 2016, it was quickly reversed following rapid intervention by global Central Banks quickly intervening with a flood of liquidity. The markets have now resumed their bullish trend currently but are pushing the limits of historical advances as noted this past weekend.

同様のことが2016年初めに生じたが、これは直ちに世界的中央銀行の迅速な介入資金注入で反転した。市場は今やこれまでのブルトレンドに戻っている、しかしこれまで何度か記事にしたがすでに歴史的に見た限界を越えている。

The Psychology Of Loss

The problem ultimately comes down to psychology.

問題は心理的失望感だ。

Last year, I wrote an article about the fallacies of “buy and hold” investing which received a good bit of push back from the community of advisors who tout that the only way to invest is to buy low-cost ETF’s and hold them long-term. As I penned:

昨年のことだが、私は「バイ&ホールド」が如何に馬鹿げているかを記事にした、投資アドバイザの間ではこの手法が良い考えだと広く知れ渡っている、投資で推奨されるのは手数料の安いETFを買って長期的に保有することだと教える。

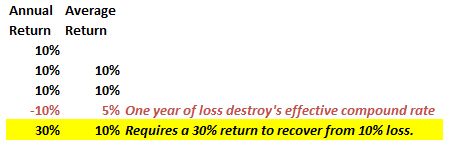

“Let’s assume an investor wants to compound their investments by 10% a year over a 5-year period.

「投資家が年率10%の複利を5年間期待したとしよう。

The “power of compounding” ONLY WORKS when you do not lose money. As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required.

「複利計算」が有効なのは損失を出さないときに限る。見ての通りだが、3年連続で10%のリターンを得ても翌年に10%の損失を出すと平均リターンは半分になる。更に言うと、これを回復するには30%のリターンが求められる。

In reality, chasing returns is much less important to your long-term investment success than most believe.”

現実的には、リターンを追い求めることは長期投資の成功ではそれほど重要ではない、多くの人はそう信じているが。」

Emotions and investment decisions are very poor bedfellows. Unfortunately, the majority of investors make emotional decisions because, in reality, very FEW actually have a well-thought-out investment plan including the advisors they work with. Retail investors generally buy an off-the-shelf portfolio allocation model that is heavily weighted in equities under the illusion that over a long enough period of time they will somehow make money. Unfortunately, history has been a brutal teacher about the value of risk management.

感情と投資判断はとても相性が悪い。不幸なことに、実際には多くの投資家は感情的に投資判断をする、投資アドバイザと共に思慮深く投資計画を実行できるひとはごく僅かだ。往々にして個人投資家は株式偏重ポートフォリオになる、長期保有すれば金儲けができるという幻想を持つためだ。不幸なことに、リスク管理を学ぶには、歴史は厳格な教師となる。

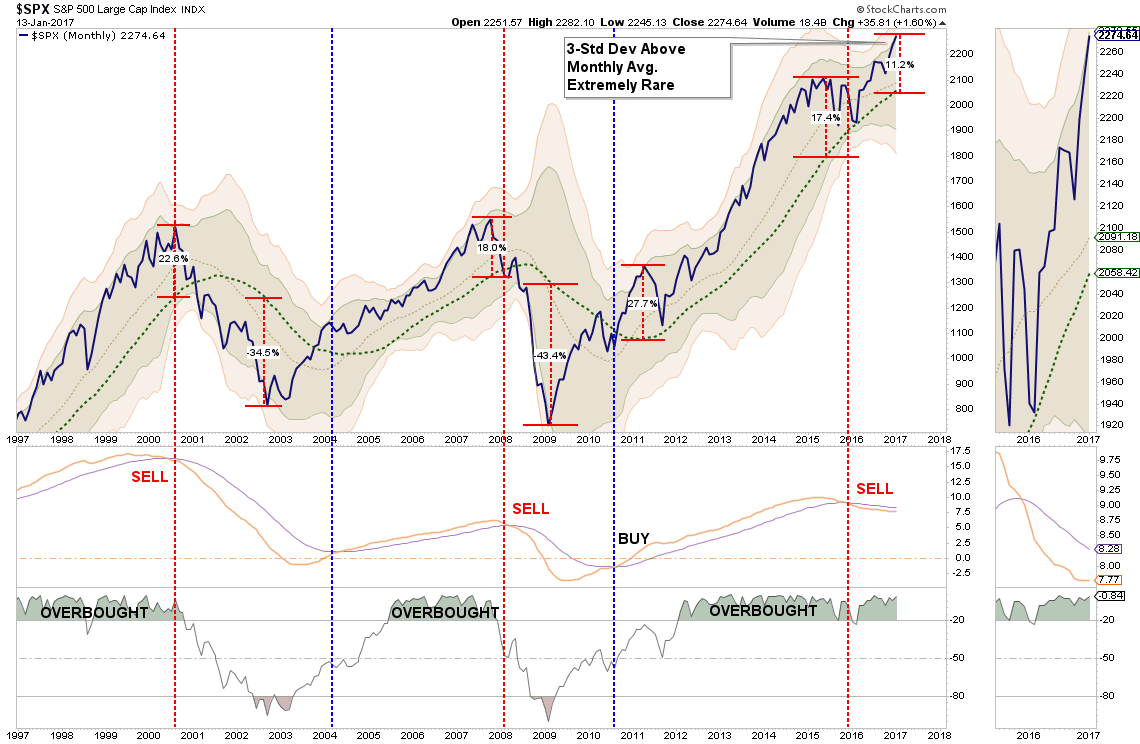

Take a look at the chart below.

下のチャートを見れば良い。

The current extension of the market above the 200-dma, combined with extremely low volatility readings and overbought conditions, have not been kind to investors over the last couple of years.

現在、株価は200日移動平均を大きく越えており、ボラティリティは極端に小さく買われすぎとなっている、この二年で見たことが無いほどのものだ。

This overbullish, overextended market is also

evidenced on a MONTHLY basis with prices currently pushing a rare

3-standard deviation extensions above the 3-year moving average.

この買われすぎ、行き過ぎ市場は月足でみても明らかだ、3年移動平均と比べた時3標準偏差を越えている。

Sure, this time could certainly be different. There is just a really high probability it will not be.

But such observations rarely deter individuals in the short-term as our emotionally driven “fear of missing out” and the now ingrained belief the “Fed won’t let the market fail,” blinds us to a multitude of psychological traps. These “traps” are the biggest reason for underperformance by investors who participate in the financial markets over time.

そう、今回は違うかもしれない。たしかにそうでない可能性も十分にある。しかしそういう見方が個人投資家へ短期的に心理的な「恐怖心の欠如」を引き起こし、そして今やすっかりとこう信じさせている、「FEDは市場下落を許さないだろう」、こうして多くの人は心理的罠に陥り何も見えなくなってします。こういう「罠」は長年金融市場に関わってきた投資家が成績を悪化させる最大の要因だ。

- Loss Aversion – The fear of loss leads to a withdrawal of capital at the worst possible time. Also known as “panic selling.”

- 損失回避ーー損失の恐怖から最悪のタイミングで資金を引き上げる。これは「パニック売り」としてしられる。

- Narrow Framing – Making decisions about on part of the portfolio without considering the effects on the total.

- 近視眼的視点ーー投資判断を長期的・全体的に見ることができない。

- Anchoring – The process of remaining focused on what happened previously and not adapting to a changing market.

- アンカリングーー以前に起きたことにとらわれてしまい、市場の変化に対応できない。

- Mental Accounting – Separating performance of investments mentally to justify success and failure.

- 心理的原因ーー投資パフォーマンスを心理的に成功と失敗に合理化してしまう。

- Lack of Diversification – Believing a portfolio is diversified when in fact it is a highly correlated pool of assets.

- 分散欠如ーー相互に相関のあるアセットを分散しているものだと勘違いしてしまう。

- Herding– Following what everyone else is doing. Leads to “buy high/sell low.”

- 群衆心理ーー他人の行動に同調する。これが「高く買い、安く売る」ことを引き起こす。

- Regret – Not performing a necessary action due to the regret of a previous failure.

- 後悔ーー以前の失敗に引きずられてそれを後悔するあまり次の適正な行動がとれない。

- Media Response – The media has a bias to optimism to sell products from advertisers and attract view/readership.

- メディア反応ーーメディアは広告主の金融商品を売るために最適化されている、そうして目を引く。

- Optimism – Overly optimistic assumptions tend to lead to rather dramatic reversions when met with reality.

- 楽観主義ーー極端な楽観主義は現実に直面すると極端に悪い結果となることがある。

The biggest of these problems for individuals is the “herding effect” and “loss aversion.”

個人投資家にとっての最大の問題は「群集心理」と「損失回避」だ。

These two behaviors tend to function together compounding the issues of investor mistakes over time. As markets are rising, individuals are lead to believe that the current price trend will continue to last for an indefinite period. The longer the rising trend last, the more ingrained the belief becomes until the last of “holdouts” finally “buys in” as the financial markets evolve into a “euphoric state.”

この2つの行動は相互作用して投資家に間違いを引き起こさせる。市場が上昇しているときには、だれもが現在の価格トレンドが永遠に続くと思ってしまう。上昇トレンドが長く続くと、より固く信じ込むようになり「確信」に変わる、とうとう市場は「euphoric state」になりとにかく「買い」となる。

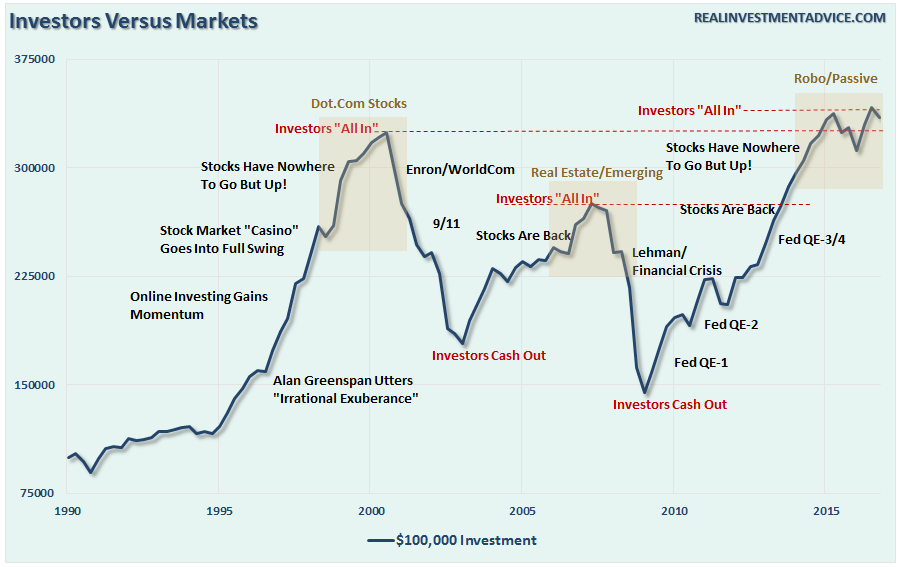

As the markets decline, there is a slow realization that “this decline” is something more than a “buy the dip” opportunity. As losses mount, the anxiety of loss begins to mount until individuals seek to “avert further loss” by selling. As shown in the chart below, this behavioral trend runs counter-intuitive to the “buy low/sell high” investment rule.

市場が下落する時、「今回の下落」は「押し目買い」の良い機会だと捉える。損失が積み上がると、損失が更に増えるのではないかと不安になり「さらなる損失回避」行動で売りとなる。下のチャートを見れば解るが、投資行動は投資の黄金率「安く買って高く売る」とは逆になっている。

Despite all of the arm waving and pounding on the table by

advisors touting long-term average returns, time-in-the-market, etc., the psychological impact of loss is all too real. While “buy and hold” investing has its appeal during bullish trending markets, the “impact of loss” on individuals is a far greater emotional pull. This is why investors tend to do everything backwards by “buying high” (greed) and “selling low” (fear).

投資顧問がテーブルいっぱいの長期投資平均リターンの資料を見せても、損失に対する心理的インパクトは現実のものだ。「バイアンドホールド」投資はブル相場の時にはよく見えるが、個人的「損失の影響」は心理的に大きな影響を及ぼす。こういう風にして投資家は「強欲で高く買い」そして「恐怖で安く売り」状況を悪化させる。

This is why managing “risk” always “wins” over the long-term by reducing the emotional pull to “do something” at precisely the wrong time. The reality of loss tends to be more than most can stomach and sentiments of “time in the market” will go mostly unheeded. This is, of course, why many of the coveted millennial investors have already rejected much of the Wall Street rhetoric after watching the devastation that wrecked their parents over the last 15 years.

というぐあいで、「リスク」マネッジが長期的な「勝利」を引き起こす、最悪のタイミングで「何か行動を起こす」という感情的投資行動を減らすのだ。現実には損失は受け入れるしか無いし、「市場のタイミングを見計らう」ことは顧みられないだろう。当然のことだが、これこそが、若い投資家が自分の両親がこの15年を台無しにしたのをよく観察して、Wall Streetの美辞麗句を拒む理由だ。

You can do better.

皆さんならもっと上手く投資できるだろう。