童話のオオカミ少年の結末をご存知でしょうか?新聞等の記事でこの言葉が使われるとき、この結末を考えた上で使っているのかどうか疑問に思う時があります。

この記事のパンチラインは難解で私には理解できません。

Weekend Reading: Time To Be A Contrarian?

Submitted by Lance Roberts via RealInvestmentAdvice.com,

In yesterday’s post, I discussed Howard Mark’s view on being a contrarian. To wit:

昨日の記事で、私はコントラリアンとしてのHoward Marks視点について議論した:確認しよう:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, particularly when momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’)

「我慢することーーそしてこれがコントラリアンとしての成功の道ーーでもこれは簡単ではない。複雑な要因が絡み合い、こういう行動を取ることを難しくしている;人というのは群れたがる性質が本来的にある、そしてその群れから飛び出すのには心理的苦痛が伴う、特にモメンタムを見ると短期的には景気サイクルに沿った行動が正しいように見える。(これが本質的なことなので覚えておくと良い「視点を遠くに設定して判断すると間違った判断との区別がつかなくなる。」)

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

将来というのは本来的に不確実なもので、今のポジションが正しいと確信するのは難しいーー特に自分が想定したのとは逆に株価が動いたときにーーこれは孤高のコントラリアンが常にその資質を試されることだ。

The important point of his comment is that being too far ahead of a turning point (either bullish or bearish), even though ultimately being proved right, is still “indistinguishable from being wrong.”

However, there is a huge difference between being making the

right call early, particularly when the trend is changing from bullish

to bearish, and making no call at all.

彼の主張の重要な点は、相場の変節点ではずっと先のことを考えることだ(これはブルにおいてもベアにおいても同様だ)、まったくもって正しい判断であっても、それでも「間違った判断と区別するのは難しい。」しかしながら、次の投資態度には大きな違いがある、事前に思いを馳せること、特にトレンドがブルからベアに変化するとき、もう一つはまったくそういうことが起きると想像だにしないこと。

The “buy and hold” mantra is essentially based on the premise that stocks rise much more often than they fall, and since you are either too stupid or lazy to actually understand how investing actually works, you are just better off making investments and forgetting about them. Hopefully, you will win.

「buy and hold」お念仏戦略は、本質的に株式というのは下落するよりも上昇することのほうが多いという前提に基いている、実際の相場がどう動くかということを理解できないほどにあなたがオバカさんか無精ものなら、投資のことなど忘れたほうがよい、触らぬ神にたたり無しだ。たぶん、逃げるが勝ちだ。

This is the equivalent of saying: “Since 8 out of 10 people who play ‘Russian Roulette’ survive the first pull of the trigger, the odds are in your favor of winning.”

これはこう言っても同じことだ:「ロシアンルーレットをする人の10人中8人は最初の引き金で生き残る、単に、勝ちに恵まれるかどうかというだけだ。」

While that is entirely true, it is the 20% of the time you lose that matters most.

これはまったくもって正しいが、大切なことは、20%は負けになるということだ。

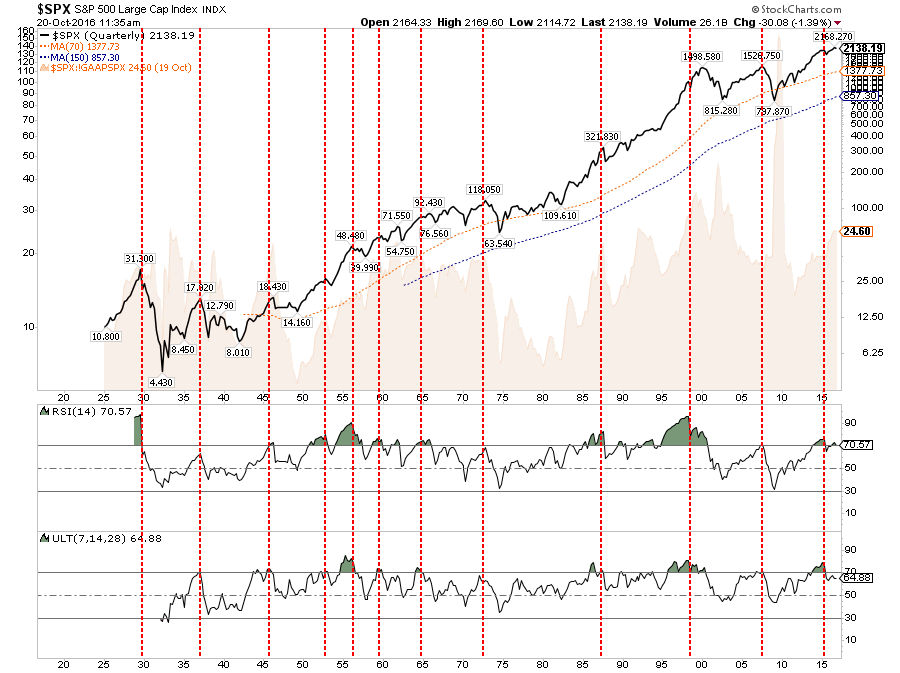

The chart below shows the long-term view of the market, going back to 1920, as compared to GAAP valuations. This

is a QUARTERLY price chart which also shows the points in history where

valuations have collided with extreme overbought conditions.

下のチャートは株式相場の長期チャートを示す、1920年来のものだ、同時にGAAPに基づくバリュエーションも示している。このチャートは四半期足であるが、バリュエーションと極端な買われ過ぎの間には強い相関があることが歴史的に解る。

While hindsight is pretty clear about what happens given the current

environment of weak economic and profit growth combined with high

valuations and deteriorating technical underpinnings, the ultimate

outcome took months to develop. Just as with the “boy who cried wolf,” warnings eventually fell on “deaf ears” at the point those warnings actually mattered.

後講釈ではあるが、現在の弱い経済と弱い企業利益が高いバリュエーションを引き起こしテクニカル分析の根拠を薄くしている、もう何ヶ月も極端な結果となっている。まさに「オオカミ少年」の警告どうり、やがて今は警告に「耳を貸さない人」にも急落が訪れる。

Currently, there is little argument the “bullish trend” remains intact. As such the mainstream analysis, if you can actually call it that, continues to the tout the inherent benefits of low cost, passive indexing and the ultimate “chase for yield.” However, it is here the real danger lies. Much of the monetary flows into passive indexes is actually NOT PASSIVE. When the eventual reversion comes, and it will, the pain inflicted on individuals, as is always the case, will turn “passive indexers” in “panicked sellers.”

It is here that being a contrarian will pay its dividends. Unfortunately, as is too often the case, there are few individuals who actually “sold high” in order to “buy low” when the real long-term investment opportunities are “laid to bare.”

現在は、「ブル相場」に関する議論は殆ど無い。主要メディアのアナリストがいつも推奨することだが、もしあなたがそれに乗るなら、低価格のパッシブ(安全)インデックス運用で利回りをもとめるだろう。「しかしながら、ここに本当の危険が待ち受けている。多くの資金がこのパッシブ(安全)インデックスに流入するということは実際には安全ではないということだ。やがて相場反転が訪れると、これは不可避だが、個人投資家に苦痛が押し付けられる、これはいつものことだが、状況は「passive indexers」から「panicked sellers」へと変わる。(訳注:音韻を踏んでおり日本語にできません。)こういうときにコントラリアンは儲けを得る。不幸なことに、あまりにもよく起こることなのだが、次に訪れる「安値で買う」良いチャンスのために事前に「高値で売る」ことのできる人はほとんど居ない、本当の長期投資の機会がそこに待ち受けているのに。

In the meantime, here is what I am reading this weekend.

話は変わり、この週末、私はこれらの記事を読もうと思っている。

Fed / Economy

- Why Won’t The Fed Raise Rates by Norman Mogil via SoberLook

- The Fed Has Made A Massive Policy Error by John Mauldin via ZeroHedge

- Draghi: So Far We So No Evidence Of Bubbles by Tyler Durden via ZeroHedge

- Zombie Banks Stalking Europe by David McHugh via AP

- Raoul Pal: A Recession Is Coming by Barbara Kollmeyer via MarketWatch

- Global Debt Exceeds Levels Of 2008 by Robert Samuelson via RCM

- Yellen: We May Not Know What We’re Doing by Jeffrey Snider via Alhambra Partners

- The LIBOR Wrecking Ball by Lisa Abramowicz via Bloomberg

- Economy: America’s Top Problem by Zac Auter via Gallup

- We Are Getting The Wrong Kind Of Inflation by Rex Nutting via MarketWatch

- Many Americans Balancing 2 or 3 Jobs by Paul Davidson via USA Today

- Economic Indicators Not Caught Up To Market by Joe Calhoun via Alhambra Partners

- Fiscal Policy: Cooking The Books by Ed Yardeni via Yardeni Research

- Subtle Forward Guidance: Best Practice by Eugen von Bohm-Bawerk via Bawerk.net

- Economy Cracking Under Too Much Debt by Adam Taggart via Peak Prosperity

Markets

- Global Debt Investors: Led To Slaughter by Danielle DiMartino-Booth via Money Strong

- The Tide Is Going Out On Stock Pickers by Rachael Levy via BI

- The Single Worst Investment Today by Brett Owens via Forbes

- Barron’s Big Money Poll: Bulls Rule by Jack Willoughby via Barron’s

- Signs Of Strain Between Stocks & Bonds by Carla Fried via New York Times

- Beware Randomly Falling Markets by David Keohane via FT Alphaville

- The U.S. Has Its Own Oil Curse by Ellie Ismailidou via MarketWatch

- Dumb Chart Predicts Crash by Paul La Monica via CNN Money

- A Better Way To Index by Ironman via Political Calculations

- Debts, Deficits & Housing: The House That Fraud Built by Aaron Layman

Interesting Reads

- Why Toxic Politics Can Foster Economic Crisis by Mohamed El-Erian via MarketWatch

- Kaepernick Or Peak Football As Ratings Decline by Stephen Carter via NY Post

- The Best Way 64% Can Boost Retirement Savings by Paul Katzeff via IBD

- Firing Line Conversation W/ James Grant by Neal Freeman via National Review

- Everything You Need To Know: Elections & Markets by Jeff Desjardins via Visual Capitalist

- 5 Books Clinton & Trump Should Read by Caroline Baum via MarketWatch

- Strange How China Keeps Posting 6.7% Growth by Leslie Shaffer via CNBC

- China’s Stable Growth & Price Of Reform by The Economist

- Fed, Damned If They Do Or Don’t by Anthony Mirhaydari via Fiscal Times

- History Will Judge Central Banks Harshly by Desmond Lachman via AEI

- Yellen & Fischer: Same Song, Same Book by Marc Chandler via RCM

- The End Of Stock Buybacks by Bryan Borzykowski via Morningstar

- The 1970’s Sans Inflation by Scott Sumner via The Money Illusion

- Don’t Wait For A Catalyst To Sell by John Hussman via Hussman Funds

- Bear Funds Go Into Hibernation by Dana Lyons via Tumblr

- How Yellen Rationalizes History’s Biggest Bubble by Jesse Felder via The Felder Report

“The only reason a great many American families don’t own an elephant is that they have never been offered an elephant for a dollar down and easy weekly payments..” — Mad Magazine

「米国家庭で象を飼わない唯一の理由はこれだ、安い値段で象が提供されることがないからだ・・・」ーーMad Magazine